| Market Cap: €9M TTM revenue: €5.4M YOY return: -89.85% |

CRO: Andreas Reif Cumulative pay: €300k (est) Shareholder value created: -€17.6M |

Forecast effort: C Forecast accuracy: B |

|

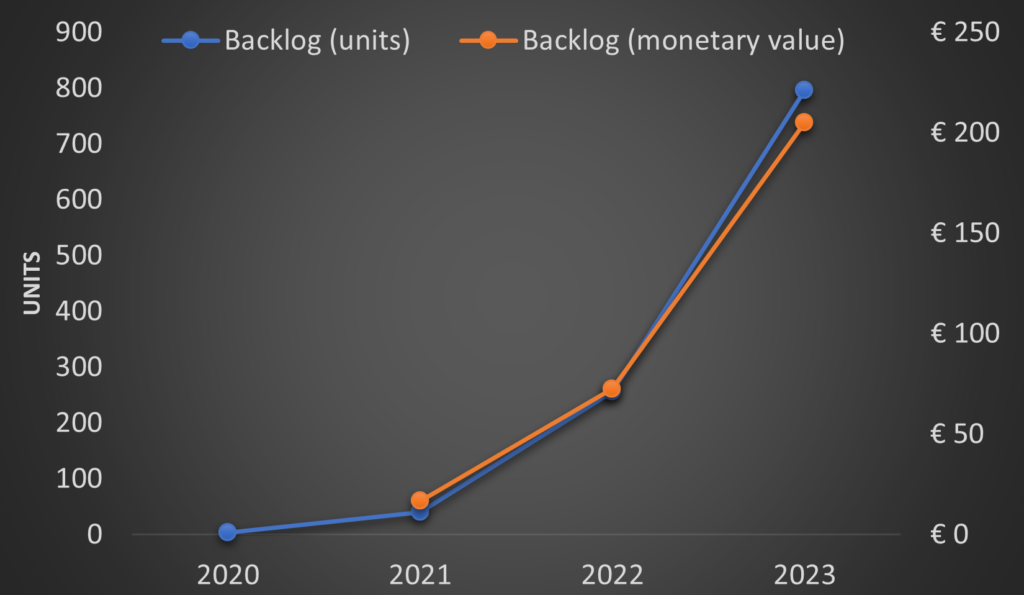

Mynaric is a one-trick pony, having successfully designed and tested optical communication terminals (i.e. lasers) enabling high-bandwidth data communication between satellites. Founded in Germany in 2009, Mynaric’s development time was long, but recently finally reached the cusp of significant revenue from mass-sales. The DOD’s Space Development Agency’s (SDA) low earth orbit (LEO) constellation already awarded contracts for 474 satellites, most of which require three of four optical terminals. Mynaric’s Condor Mk3 optical terminal meets SDA’s required spec. Largely from sales of Condor Mk3s to SDA contractors, Mynaric built a sales backlog of nearly 800 units worth approximately $170m.

But in 2024, things turned south. In May 2024, Telesat announced choosing Mynaric-rival TESAT for supply of 792 optical terminals for its LEO Lightspeed constellation. Then in August, Mynaric announced low production yield and supply chain shortages would widen operating losses and that it required additional cash. Mynaric’s stock price tanked, falling as much as 80% before slightly restabilizing. Mynaric subsequently obtained some limited financing, but their ability to manufacture, delivery, and keep their orders remains unproved. Beyond that, Mynaric is delinquent in its financial reporting. Mynaric then announced plans to peruse court-authorized restructuring, which could result in shareholders losing all their investment.

2 Minute Version

- Mynaric (NASDAQ:MYNA)(FRA:M0YN) trades publicly in Germany, first going public on the Frankfurt Stock Exchange in October 2017. In 2021 they deposited shares in the United States which trade on the NASDAQ, four of which are equivalent to one German share.

- As of 2023, Mynaric’s primarly revenue source is sales of Condor Mk3 optical terminals to United States based customers. The Condor Mk3 is an Optical Inter-Satellite Link (OSIL) – or what Elon Musk refers to as “space lasers.” OSILs enable high-bandwidth communication between satellites.

- Satellite internet constellations use OISLs to create a communication network between satellites. This allows satellites out of range of ground stations to communicate with the ground network by relaying data through other satellites.

- The largest user of OISLs is SpaceX’s Starlink constellation, which uses OISL’s developed and made in-house by SpaceX.

- The SDA is the second largest OISL user. SDA requires OISLs to adhere to a published specification before use on its satellites. SpaceX OISLs do not currently meet SDA’s specification. Mynaric’s Condor Mk3 is SDA compliant.

- SDA to-date has awarded 22 contracts for 474 satellites, the majority of which require three or four OISL terminals installed on each satellite.

- SDA satellites appear the largest source of Mynaric’s sales. Mynaric entered agreements to supply Condor Mk3 terminals to SDA contractors Northrop Grumman, Raytheon, Ball, and Rocket Labs. (Raytheon’s contract later terminated.)

- Competition is fierce. Airbus subsidiary TESAT, CACI, and Skyloom each offer their own SDA-complainant OISLs.

- Nonetheless, Mynaric built a backlog of 796 terminals. Mynaric sells Condor Mk3 terminals for between $214k and $277k. Mynaric values its backlog at €205m.

- Telesat is likely the third largest OISL user, but opted to order 792 units from Mynaric competitor TESAT in May 2024.

- In August 2024, Mynaric dropped a bomb that production yields and supply chain issues would negatively impact shipments, revenue, and margins. These production problems arose after former CEO Bulent Altan told the press Mynarics’s “underlying technology is really mass production oriented.”

- Without sufficient cash to maintain operations, Mynaric secured additional loans in October and November 2024. Mynaric also announced improving production yields and its supply chain issue. But Mynaric’s ability to meet delivery obligations and maintain margins with high production yields remains to be seen.

- No customers have announced order cancellation, but similarly no new customers have announced procurement from Mynaric since August 2024.

- In December 2024, Mynaric announced it may pursue restructuring under German law (StaRUG). Mynaric warned investors such restructuring could eliminate part or all of their investment.

Financial Disclosures

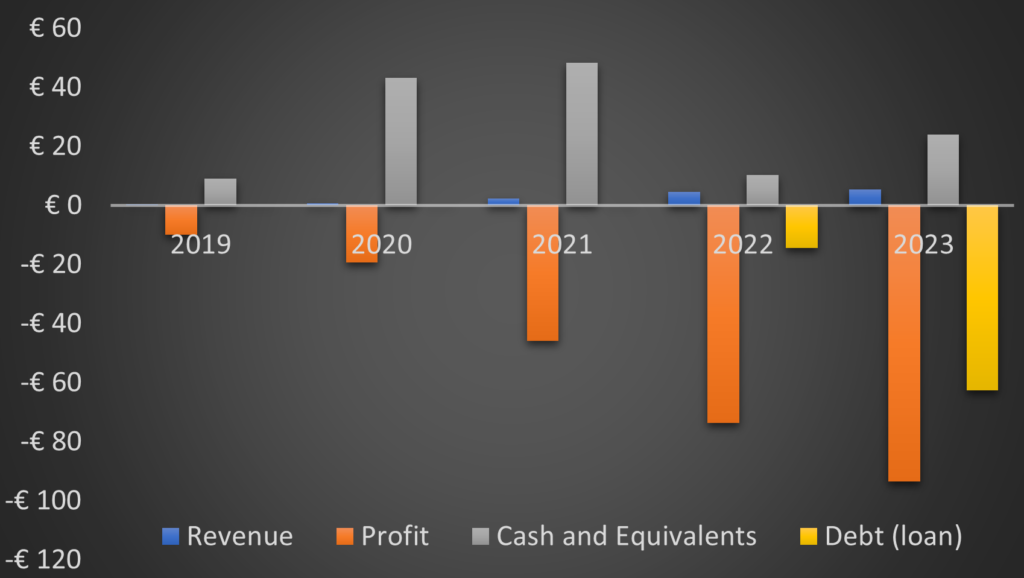

There is little to see from Mynaric’s annual and quarterly financial results. Revenue has been flat, near-zero while Mynaric has invested in its optical link development. Operating losses in 2022 and 2023 both exceeded management’s prior forecasts. 2024 is on track to repeat with operating losses topping management’s forecasts a third straight year.

Mynaric first went public in Germany on October 30, 2017, raising €27.3 million in an oversubscribed IPO. Four years later in November 2021, Mynaric deposited shares on the U.S. NASDAQ, raising an additional $75.9m. By end of 2022, Mynaric expended its U.S. IPO proceeds and began taking on debt. In 2023, Mynaric took on more loans apparently in anticipation of manufacturing scale up and revenue realized from its large order backlog.

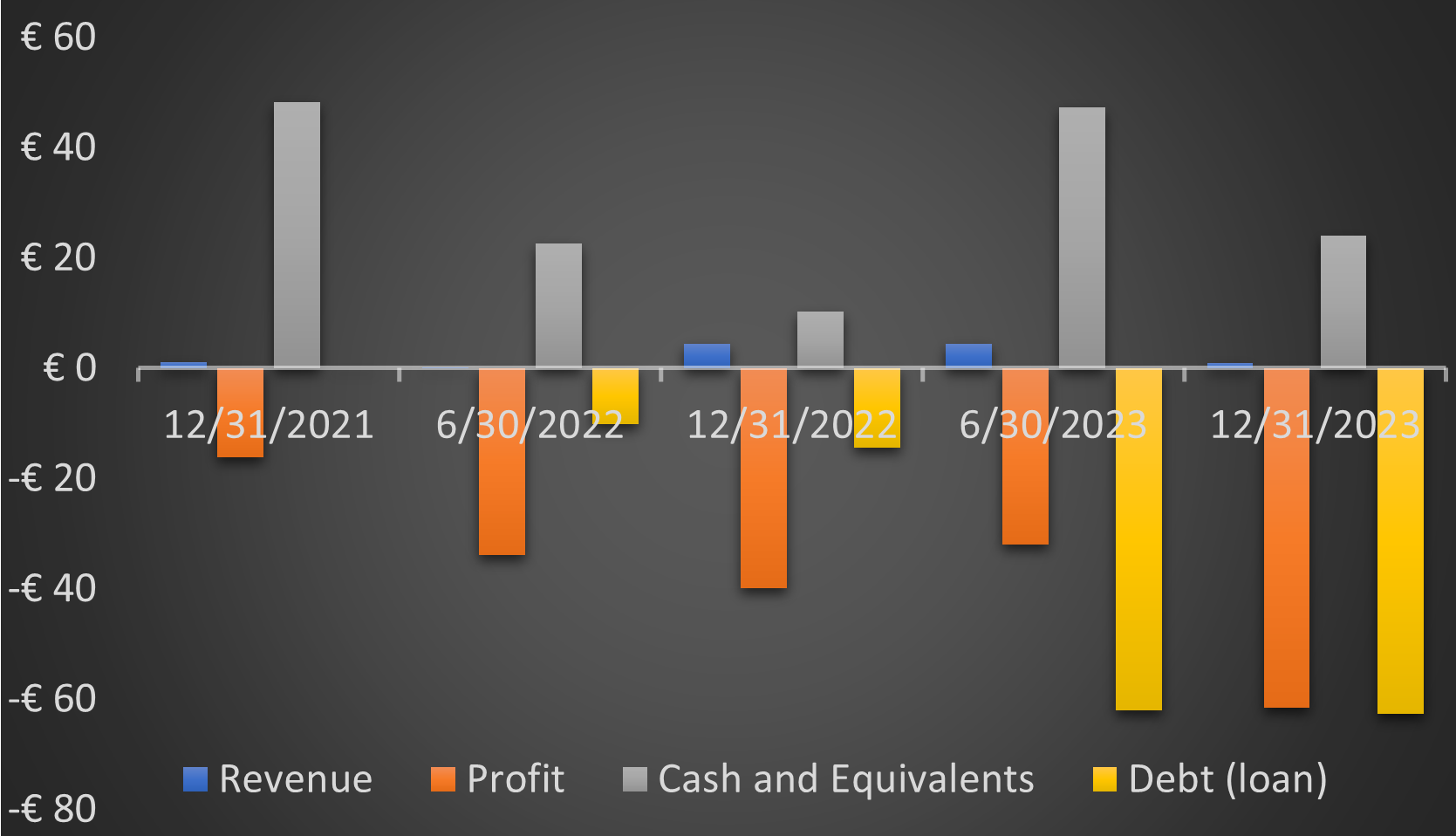

As a foreign issuer, Mynaric reports semiannually as opposed to quarterly. In August 2024, Mynaric infamously announced its production problem and need for additional capital. Mynaric took on more debt in 2H of 2024. (Not reflected in chart below. Mynaric is currently delinquent on its financial reporting.) Prior to Mynaric going public with its production problems, its most recent posted financial period was 2H 2023 when Mynaric had both record debt and record losses. Investors await, (1) Mynaric getting current on its financial reporting, and (2) evidence backlogged revenue may lead to operating income.

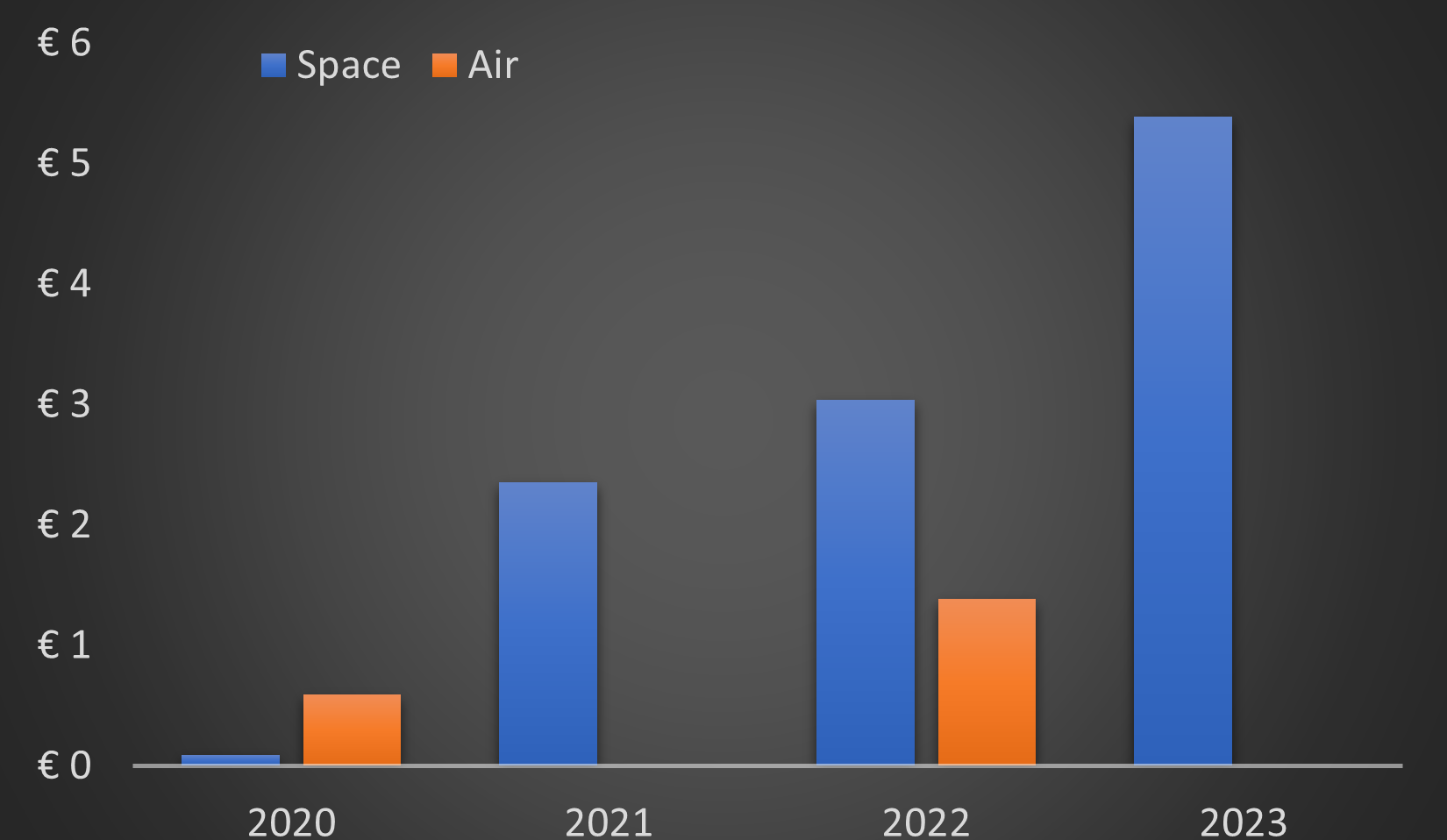

In additional to satellite OISLs, Mynaric simultaneously developed optical terminals enabling aircraft to connect with the ground. Whereas Mynaric recognized some revenue from its air segment in 2020 and 2022, this apparently died out. Mynaric’s business future appears fully married to successful sales to satellite customers.

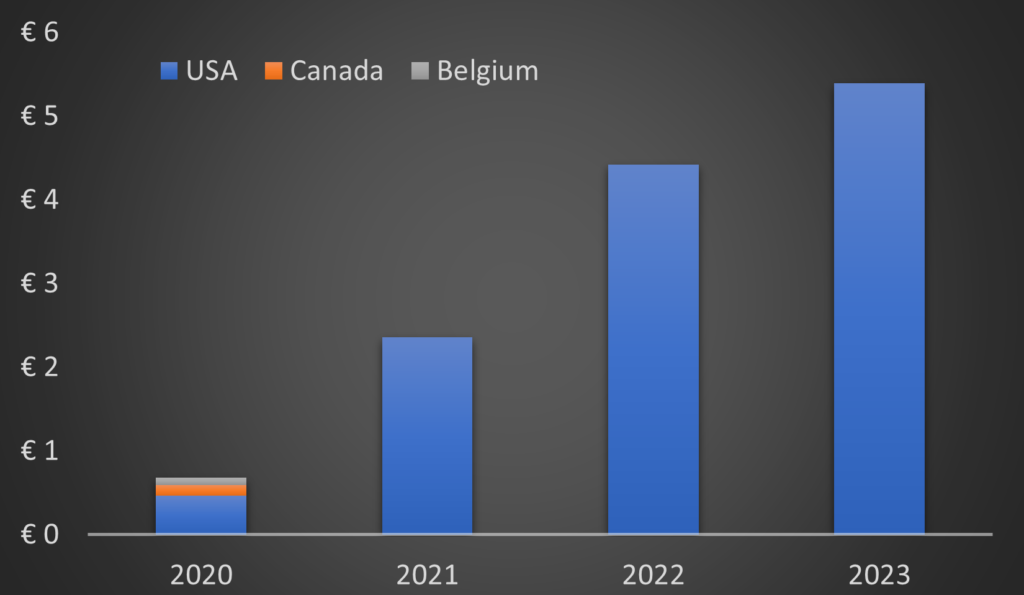

Similarly, Mynarics future also appears married to the United States. In 2020 Mynaric recognized some revenue from customers in Canada and Belgium. And in 2019 revenue was reported from the UK. But since then, all revenue sourced from the USA.

Mynaric’s reliance on U.S. sales seems set to continue. Mynaric’s customers include:

- Capella Space, a SAR satellite operator selling imagery to the U.S. government. Mynaric’s OISLs will enable near real-time transmission of imagery through satellite networks without need to wait for Capella’s satellite to pass over a ground station. (Blacksky‘s Gen-3 satellites similarly will launch with OISLs, but their OISL supplier remains undisclosed. )

- Rocketlab selected Mynaric to supply Condor Mk3s for its SDA Tranche 2 contract.

- Northrup Grunnman also inked deals with Mynaric to buy Condor Mk3s for the satellites it makes for the SDA.

- Mynaric also had a deal with Raytheon to supply Condor Mk3s for its seven SDA satellites. But the SDA cancelled its satellite contract with Raytheon.

- Mynaric also supplies Condor Mk3s to Loft Orbital satellites built for the SDA.

- Mynaric also supplies its OISLs directly to the SDA for a ground station used to connect optically with satellites in orbit.

Backlog

Mynaric’s backlog is impressive. At end of 2023, management reported a 796 unit backlog worth €205m. As of December 31, 2023, Mynaric reported contract liabilities and liabilities due to customers totaling 58.9m Euro. Thus apparently customers have pre-paid approximately 29% of Mynaric’s backlog, which Mynaric has not yet recognized as revenue. Clearing the current backlog thus offers approximately €146m is cashflow. 2023 operating cashflow totaled -€29.0m, so the potential cashflow from clearing backlog is comparably huge.

Costs, margins, and potential future profitability

However, potential margins per Condor Mk3 are the wildcard. Prior Mynaric CFO Stefan Berndt-Von Bulow stated in 2024 that Mynaric was seeking 50% gross margins. However, his statement seemed to suggest 50% as a mid- to long-term goal once material costs later reduce. A 2021 report by Pareto Securities AS, paid for by Mynaric, earlier targeted 40% gross margins in 2025. Being that management historically overstates its forecasts, and Mynaric announced higher production costs from lower yields in August 2024, investors likely should conservatively model near term gross margins under 40%. Assuming 25% gross margin rate, if Mynaric overcomes its production challenges and clears its backlog in two years, this results in approximately €51.3m gross profit. Likely not enough. Mynaric’s other operating costs (not included in COGS or gross margin calculations) totaled €23.2m. So 25% gross margins and clearing all backlog in two years, may only get Mynaric to break even (if they control costs).

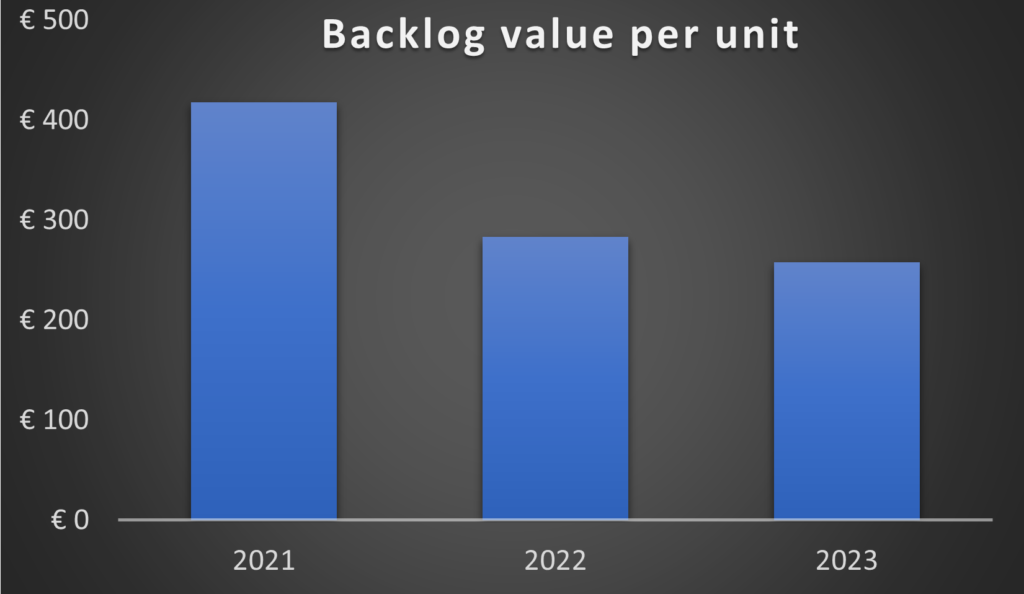

However, financial data suggests Mynaric’s selling price is eroding while internal personnel cost rise. These trends undoubtably will further pressure gross margins. As seen in the above chart, Mynaric’s backlog per unit OISL is growing faster than backlog monetary value. This necessitates that Mynaric’s selling price per unit OISL is decreasing. Plotting for the three years for which data is available indicates Mynaric’s average sales price per unit has deceased from €418k in 2021 to €258k in 2023.

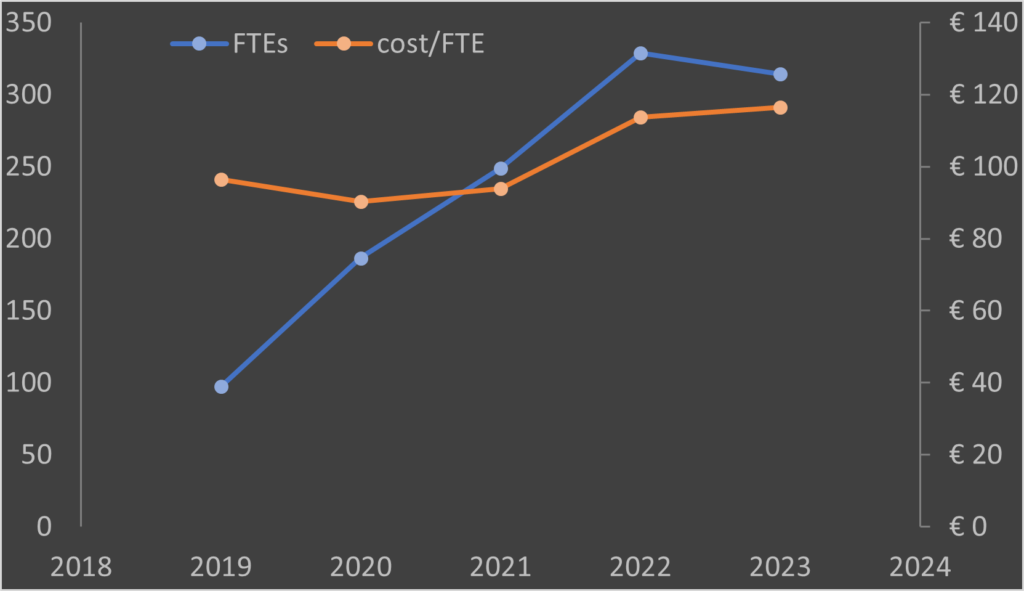

Conversely, Mynaric’s internal personnel labor costs trend upwards. Mynaric reports number of full time employees and total personnel costs. Total headcount dipped between 2022 and 2023. But salary related costs per employee rose from €93,873 in 2020 to €116,499 Euros in 2023.

Competition

The competition for supplying OISLs to SDA satellite contractors is intense. Currently SDA is the largest OSIL customer (aside from Starlink “buying” its own OISLs from SpaceX). Mynaric, Airbus’s TESAT, CACI’s SA Photonics, and Skyloom each have SDA conforming products. General Atomics also tested its OISLs in orbit in partnership with the SDA. And Space Micro is developing its own OISL, partially supported by a SDA-funded contract.

Honeywell/Ball and French-based Thales offer their own OISL satellite terminals, but the later is not known to meet SDA spec. (Thales’s OISL was planned for use on the Lightspeed constellation before Thales lost its satellite contract to MDA.)

Telesat selected Mynaric rival TESAT to provide 792 OISLs – roughly the equivalent to all of Mynaric’s current total backlog – for Lightspeed. This single order likely is worth approximately $170m. Potentially concerning is Telesat selected TESAT after previously buying and using Mynaric’s Condor Mk2 on another mission.

Not to be forgotten, SpaceX is the world’s largest manufacturer and OISL user. SpaceX apparently ignored SDA’s spec and designed its own standard. At Satellite 2024, SpaceX announced it would sell its OISLs as a standalone product. So far there are no announced customers. Amazon too, instead of buying from a third-party, developed its own OISLs for its Kuiper constellation. These successfully performed in orbit in October-November 2023.

Oneweb’s 1st Gen satellites did not use OISL’s but their second generation satellites planned to launch with them. However this now seems scrapped/delayed as Oneweb operator Eutelsat will use bandwidth from IRIS2 to sell to Oneweb customers.

The EU’s IRIS2 constellation will utilize OISLs, and only EU-based firms are eligible to bid on the supply contract. This is favorable for Mynaric, narrowing its competitors to Thales and TESAT.

Kepler Communications also plans OISLs for its 18 satellite constellation. Kepler also selected TESAT OISLs for its satellites.

Finally, Rivada’s 600 satellite LEO constellation also plans OISL-based inter-satellite connections. The design calls for four OISL terminals per satellite, suggesting a total of 2400 OISLs in Rivada launches all 600 satellites. Whether or not Rivada funds and launches is another question, but if it does, this OISL supply contract could value around $500m.

Aside from major customers Telesat and Kepler selecting TESAT’s OISLs, Mynaric faces risk of losing business from its manufacturing problems announced in August 2024. Mynaric’s manufacturing issues resulted in negative press reports which suggested Mynaric could threaten delaying SDA satellite production. Competitor CACI stated in response that they could fill orders with their own product. Clearly articulable risk exists of Mynaric eroding existing backlog if they cannot meet delivery requirements.

Summer 2024 mass-production failure

The issue which could lead to Mynaric’s end as a public company is a manufacturing failure experienced in summer 2024. As far back as November 2021, prior CEO Bulent Altan boasted Mynaric’s “underlying technology is really mass production oriented.” In June 2023, then Mynaric Co-CEO Mustafa Vezirogku represented Mynaric had invested in manufacturing capability allowing Mynaric to give confidence to customer that “we will be able to meet their needs.” Mustafa stated concerning large constellation customers requiring OISLs: “Last thing the company investing $2, $3 billion dollars for their constellation want to worry about is will these guys whom I am counting on for laser communication be able to deliver to me the kinds of quantities that I need. The answer obviously for us is ‘yes, we can.'” Mustafa further stated Mynaric already had capacity in place to product 2000 Mk3 Condors per year. Well, mass production did not turn out to be so easy as Mynaric’s prior CEOs held it out to be.

In August 2024, Mynaric disclosed low production yields and supply chain issues would negatively impact shipments. Decreased production yields also meant lower margins than forecasted. And delayed shipments meant delayed cash incoming from customers. These issues forced Mynaric into requiring additional capital to maintain operations. Mynaric stock lost 68% of its value following the news. Within a week, Mynaric terminated prior CEO Mustafa Vezirogku.

Then in September, Mynaric announced seeking “additional capital sources to secure [its] on-going operations and production ramp.” Mynaric received loans in October and November 2024, but these loans were short-term. (A bridge loan announced in October matured a month later. And in November Mynaric received a bridge loan maturing at end of December.) All this happened while Mynaric aimed to receive additional pre-payments from a large customer under a “production increase incentive agreement.”

Sadly, in December, Mynaric announced the lender of its bridge loans would only continue funding if Mynaric reorganized under the German StaRUG Act. StaRUG is in large part similar to U.S. Chapter 11 Bankruptcy. Mynaric advised it viewed StaRUG reorganization as likely, warning, “this could result in shareholders losing part or all of their investment.” Mynaric stock lost 73% of its value on this news.

Management guidance scorecard

Through 2023, Mynaric’s guidance record was fairly commendable. Although guidance generally was not multiyear, Mynaric managed to hit management’s forecasts. This however lasted until it became time to scale up and deliver product.

Management stopped providing guidance in 2024 when Mynaric became delinquent with its financial reporting.

Chief Restructuring Officer Andreas Reif compensation

Andreas Reif has served as Chief Restructuring Officer of Mynaric since prior CEO Mustafa Veziroglu’s employment terminated in August, 2024. Andreas Reif’s salary is unknown as his his share holdings. Prior CEO Veziroglu’s 2023 salary was €853,000 for 11 months of 2023. Thus Reif’s salary is likely no greater than this amount. The stock price under Reif’s helm has fallen, something that arguably may not have been preventable considering the number of issues he inherited.

Mynaric outlook and risk assessment

Mynaric is in immediate danger. If they don’t obtain extension of their current bridge loan or replacement financing, it could be over. They warned that no replacement financing option appear available. And pending StaRUG restructuring could zero out shareholders’ existing equity. Mynaric warns as much. The provider of the current bridge loan will only extend the loan if restructuring appears likely. Even if Mynaric survives restructuring and shareholders retain some equity, the future still is far from guaranteed. This is as risky as it gets.

What to look from Mynaric

Funds associated with an undisclosed U.S.-based global investment management firm have loaned Mynaric $21.5m since October 2024. These loans may be terminated early if a precommissioned restructuring expert opines that it is no longer more likely than not that Mynaric is capable of being restructured. Mynaric plainly warns:

“Currently, it is envisaged that the restructuring plan will provide for a reduction of the Company’s share capital to zero followed by a capital increase excluding statutory subscription rights. Accordingly, the StaRUG proceedings may result in shareholders losing all of their investment in the Company. Other financing opportunities for the Company are currently neither available nor in sight.”

Restructuring, which apparently appears more likely than not, could very well result in shareholders losing all of their investment. The restructuring plan aims to eliminate the current shareholders’ ownership (by reducing share capital to zero) and then issue new shares to new investors (or perhaps a select group of existing ones) without giving the old shareholders a chance to participate.

It appears current shareholders are betting on (1.) new financing appearing, which Mynaric suggests is unlikely, or (2.) the court retaining some of existing shareholders’ ownership in the restructuring plan, which is contrary to the restructuring plan being offered.

Recent News

-

Mynaric after NASDAQ delisting and manufacturing yield issues sends team to Satellite 2025

Mynaric (FRA: M0YN) has a booth at Satellite 2025, apparently to drum up sales. Six months delinquent on financial reporting, delisted from the NASDAQ, and…