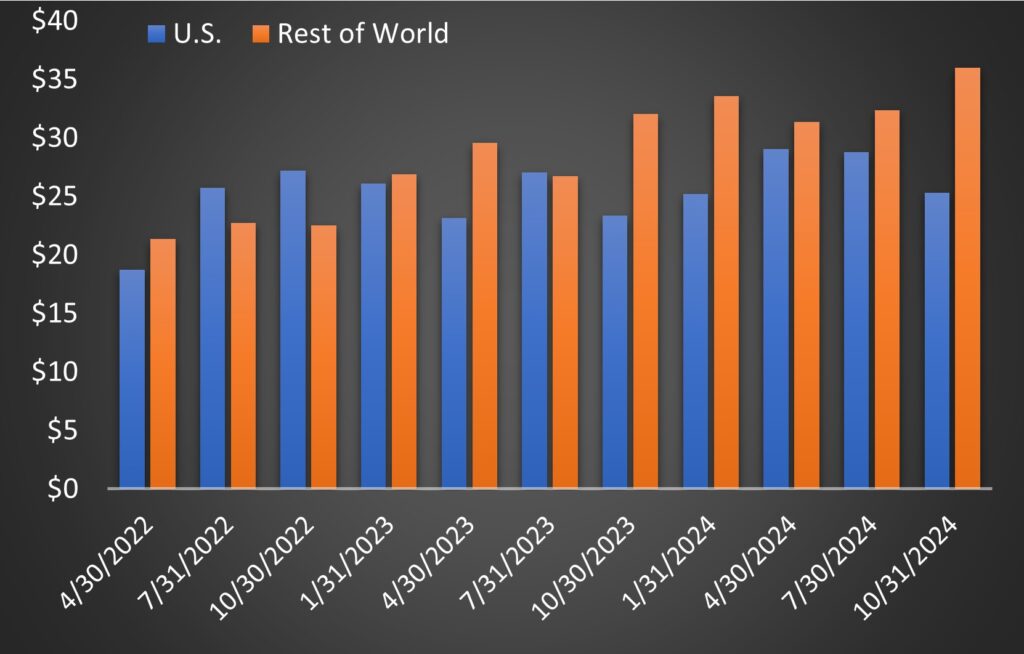

Planet Labs (NYSE: PL) released its Q3 financial results for 2025, which were largely in line with projections. The company operates on a calendar year with fiscal years ending January 31. Following the announcement, there was no significant stock price fluctuation. Planet Labs continues to experience growth in foreign revenue, which has increased by 60% over the past two years, while domestic sales have declined by 7%. Currently, foreign revenue accounts for 59% of Planet’s total business. It’s important to note that these foreign accounts may be particularly vulnerable to competition from future low-cost satellite operators; however, this competition is not expected to materialize for at least another two years, allowing overseas sales to fuel Planet’s slow but steady growth for the time being.

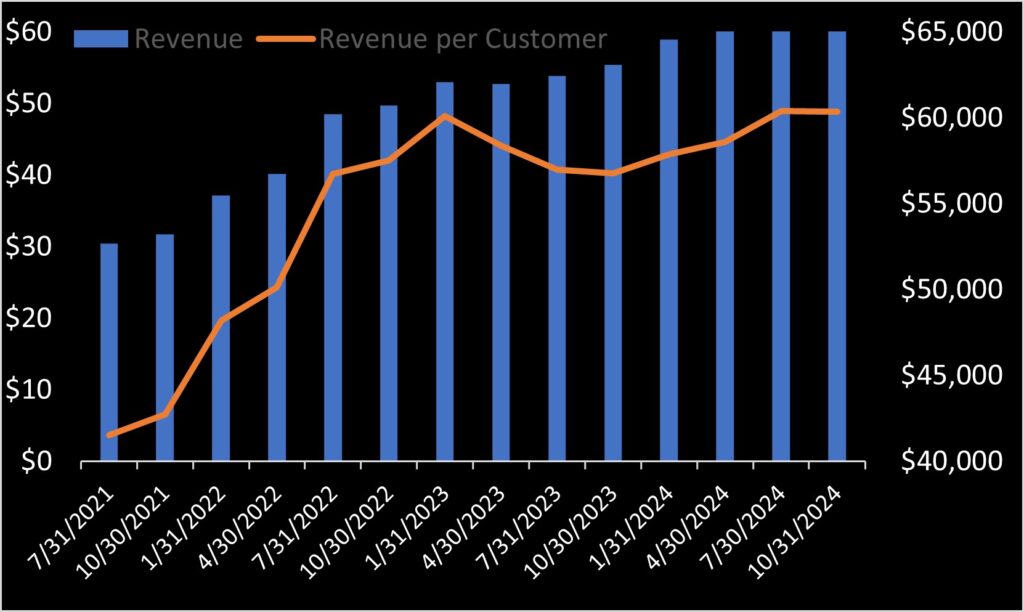

After three consecutive quarters of growth, revenue per customer stagnated in Q3. Although the total number of customers grew by 40% from summer 2021 to January 2024, it has plateaued for the past four quarters. This may suggest that Planet has reached market saturation. Management attributes this to the elimination of low-quality customers; however, the data does not support this claim, as one would expect revenue per customer to increase if lower-quality accounts were removed. Instead, it has not increased since 4Q 2023 (ending January 2023).

Despite this stagnation, Planet Labs managed to reduce its quarterly loss and cash burn in Q3. The company holds $242.2 million in cash and short-term investments. The net loss for Q3 was $20.1 million, the smallest since going public, with $11.8 million of that attributed to stock-based compensation. Excluding this compensation, Planet would have reported a loss of $8.3 million last quarter.

Looking ahead, Planet forecasts reaching positive EBITDA in Q4, which seems attainable. The company posted an EBITDA of just -$242,000 in Q3, so even a slight improvement will lead to positive EBITDA in Q4.

It appears the layoffs significantly slowed the cash bleed. Planet’s decrease in losses are not result of topline growth. Planet’s cash position is now stronger than it was just a quarter ago, with enough funds to sustain three years of operations at the Q3 loss rate. For context, in Q2, Planet’s cash reserves were sufficient to cover six quarters of losses at that time.

Finally, Planet Labs’ stock has benefited from a favorable post-U.S. election run, experiencing a sharp rise since election day. Even after a retreat, it is trading 80% higher than on election day.