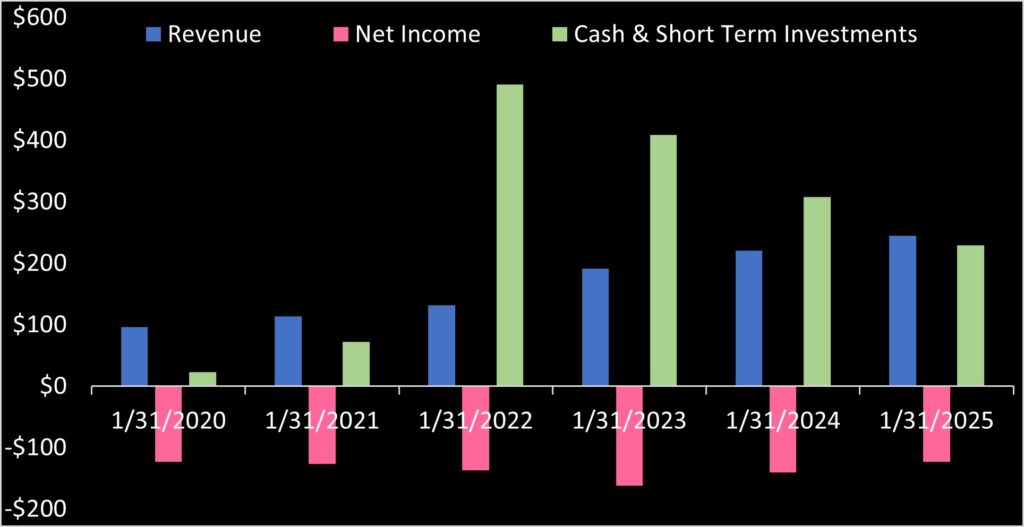

Planet Labs (NYSE: PL) released 2025 forth quarter financials (for fiscal year ending January 31, 2025) showing annual revenue grew 10.7% YoY. Planet added guidance that revenue will grow by as little as 6.4% this fiscal year, and by twice that rate the following year. Planet’s efforts to reign in costs are noticeable nut have not produced significant reductions to net loss. Planet still holds $228 million in cash from its wildly successful IPO. This should fund operations for roughly 2 years at current burn rates. However, coincidently Planet now forecasts reaching positive cashflow within 24 months. If this turns out true, Planet likely needs no further funding to reach profitability. We analyze.

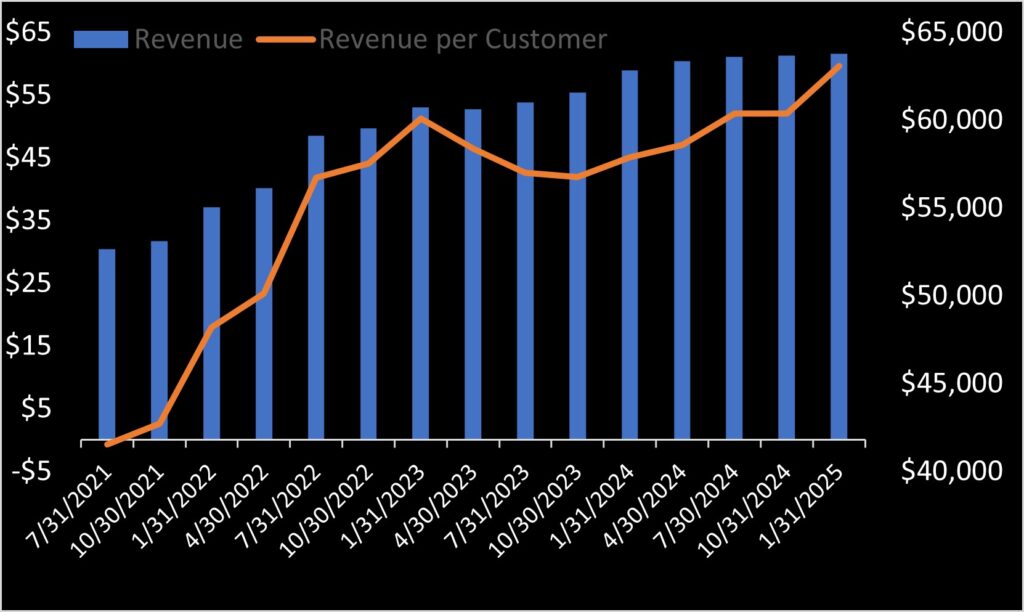

Planet continues disclosing total customers. Using this metric with revenue, Planet’s revenue-per-customer reached an all-time high. Total customers peaked at 1031 in first quarter 2025. Whereas this has fallen to 976, total revenue per customer now reaches $63,000. Whether this is due to Planet’s customers increasing spend, or Planet shedding low-quality accounts, the data is not clear.

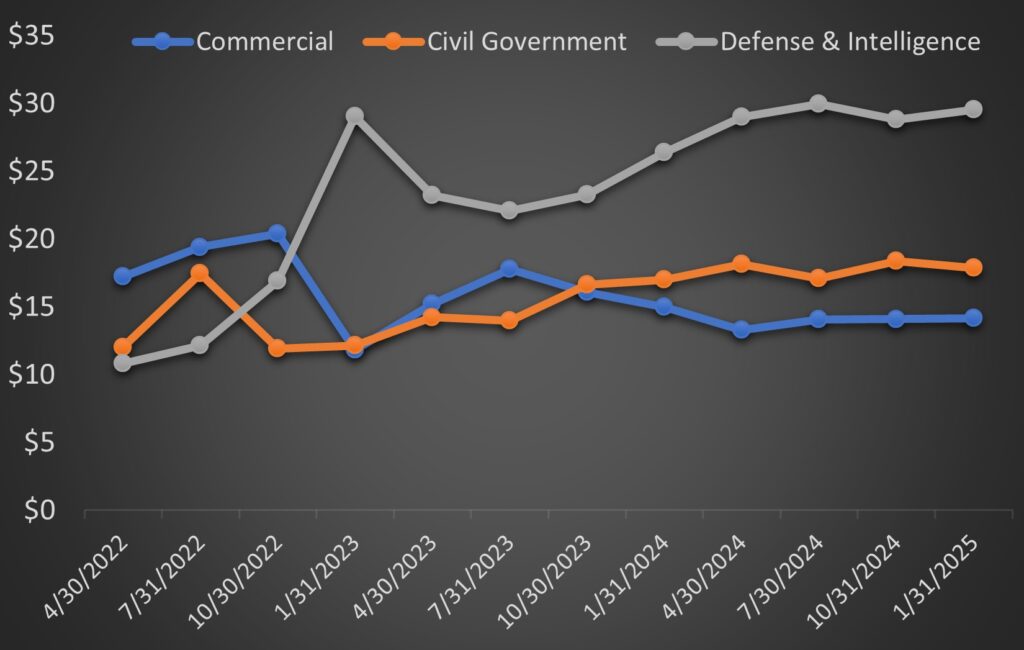

Sales to defense and intelligence customers remain Planet’s largest market, rebounding from last quarter and nearly mirroring highs set two quarters ago.

Company’s projections and future break-even

CEO Will Marshall stated in Planet’s release that he sees “a clear path to at least double our revenue growth rate in FY’27 compared to FY’26.” Planet projected 2026 revenue to fall between $260 and $280 million. This represents YoY growth of between 6.4% and 14.6%. If Planet achieves its projected FY26 revenue and doubles its growth rate the following year, this implies FY2027 revenue will fall between $293 and $361.8 million.

Assuming the recent quarter’s operating cost structure remains constant (it actually is improving by trending downward), we can calculate required revenue for Planet to reach operational profitability. Last quarter’s gross margin was 62%. Full year FY25 gross margin was 57%. Assuming 57% gross margins, Planet needs $404.2 million in revenue to reach breakeven. This exceeds the top end of Planet’s forecasted revenue.

However, gross margins include stock-based compensation, amortization of acquired intangible assets, and restructuring costs. The first two are non cash expenses and totaled $1.6 million last quarter. And the last is presumably a non-reoccurring charge. Discounting these, Planet needs about $384 million revenue for yearly breakeven. This is just outside of the upper range of management’s forecast.

Planet carried $93.4 million in deferred revenue at end of FY25. This is up from $77.6 million as of the end of FY24. Thus growing pre-payments from customers could help push Planet into positive cashflow.

In a technical sense, Planet may not have forecasted reaching positive cashflow in 24 months. The actually quote is “we believe we have line of sight to cross over to positive cash flow in the next 24 months.” If Planet by “line of sight” means the math supports reaching positive cashflow, this appears to be justified using Planet’s achieved margins and the top line of their revenue guidance.