| Market Cap: ¥79.8B TTM revenue: ¥2.3B YOY return: +9.19% |

CEO: Motoyuki Arai Cumulative pay: ¥2M (est) Shareholder value created: ¥24.1B |

Forecast effort: C Forecast accuracy: F |

|

Synspective (TYO: 290A) is one of five small Synthetic Aperture Radar (SAR) satellite operators, with high resolution SAR satellites already proven in orbit. Synspective aims to operate profitability after reaching 10 satellites in its constellation by 2026. At the time of IPO in December 2024, Synspective had three satellites. The IPO (with overallotment) successfully raised approximately 11.9b yen (~$75m). Management forecasts building and launching each satellite will cost ¥2.5 billion ($15.6m) making Synspective more expective than its competitors. Thus Synspective IPO proceeds alone will not be sufficient for Synspective to reach profitability. Synspective intends using commercial bank loans and potentially satellite revenue to fund its constellation.

2 Minute Version

- Five small satellite companies currently compete to provide SAR imagery predominately to government customers. Umbra and Capella operate from the United States. ICEYE headquarters in Finland. And Synspective and iQPS are from Japan. All and currently building and launching out their planned constellations

- Synspective’s satellites offer SAR imagery with resolution reaching up to 25cm. This betters domestic competitor iQPS. However, Synspective lags small sat leader Umbra who reports offering up to 16cm commercial resolution.

- Synspective plans 30 satellites and 46% operating profit margin by 2028.

- Synspective’s business plan reaches profitability in 2026 once its constellation reaches 10 commercial satellites. The business plan predicates on SAR imagery prices not declining. Whether prices hold as Synspective and their competitors all increase their imagery capacity multiple-fold remains an important open question.

- Synspective’s business model highly depends on Japanese defense sales. It calls for 80% Japanese defense sales in 2026 with 11 satellites in orbit, dipping to 60% in 2028. Domestic competitor iQPS’s business model similarly also heavily depends on Japanese domestic defense sales.

- The Japanese Ministry of Defense (MOD) budget for satellite imagery currently is too small to support Synspective’s 2028 business plan. Significant Japan MOD imagery budgetary growth is required to support Synspective’s business plan.

- Likely Synspective will need to find international sales traction quicker than currently planned.

- Synspective represents greater than 90% of 2023 sales originated from Japan. This suggests that some sales (<10%) are foreign-sourced. On this point Synspective appears to be a step ahead of domestic competitor iQPS which appears fully Japan-dependent on revenue.

- Synspective reports the highest cost to manufacture each satellite among the five small SAR satellite providers.

- At time of IPO, Synspective traded with an approximate market cap of $390m while projecting $14.5m revenue and $19m operating loss for 2024. Converse with (optical) imagery provider Blacksky (NYSE: BKSY), trading with market cap of $340m and projecting $102m revenue and +$8m EBITDA in 2024. It is not difficult to see why Synspective may be comparatively overvalued.

Financial Disclosures

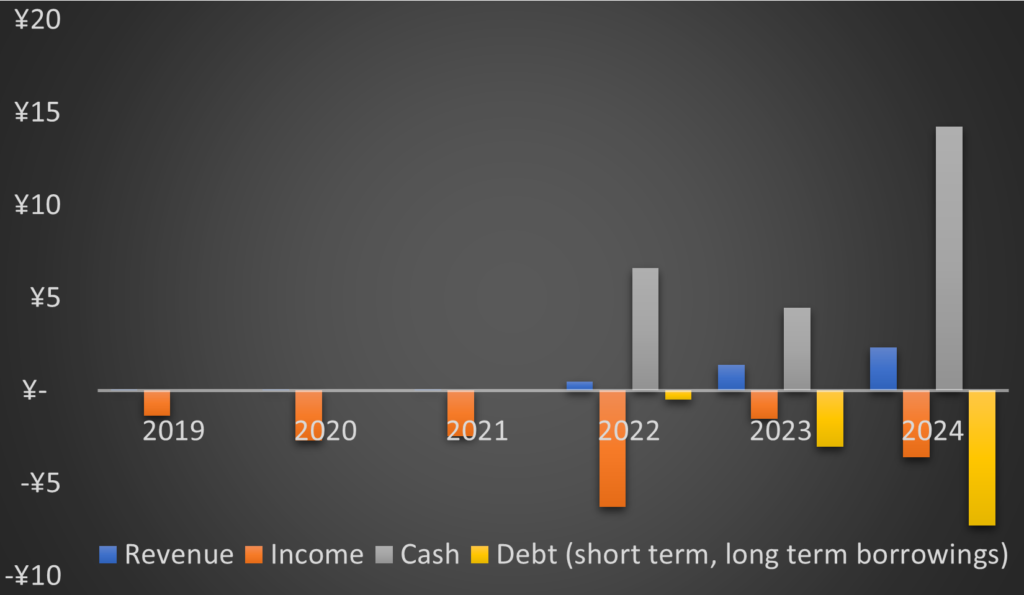

Synspective’s annual financials shows little other than Synspective is a early growth company. Cash holding and debt balances prior to 2022 are unknown. Historical quarterly reporting is also unknown. Presently 2024 Q4, Q3 and partial data for Q2 2024 is public.

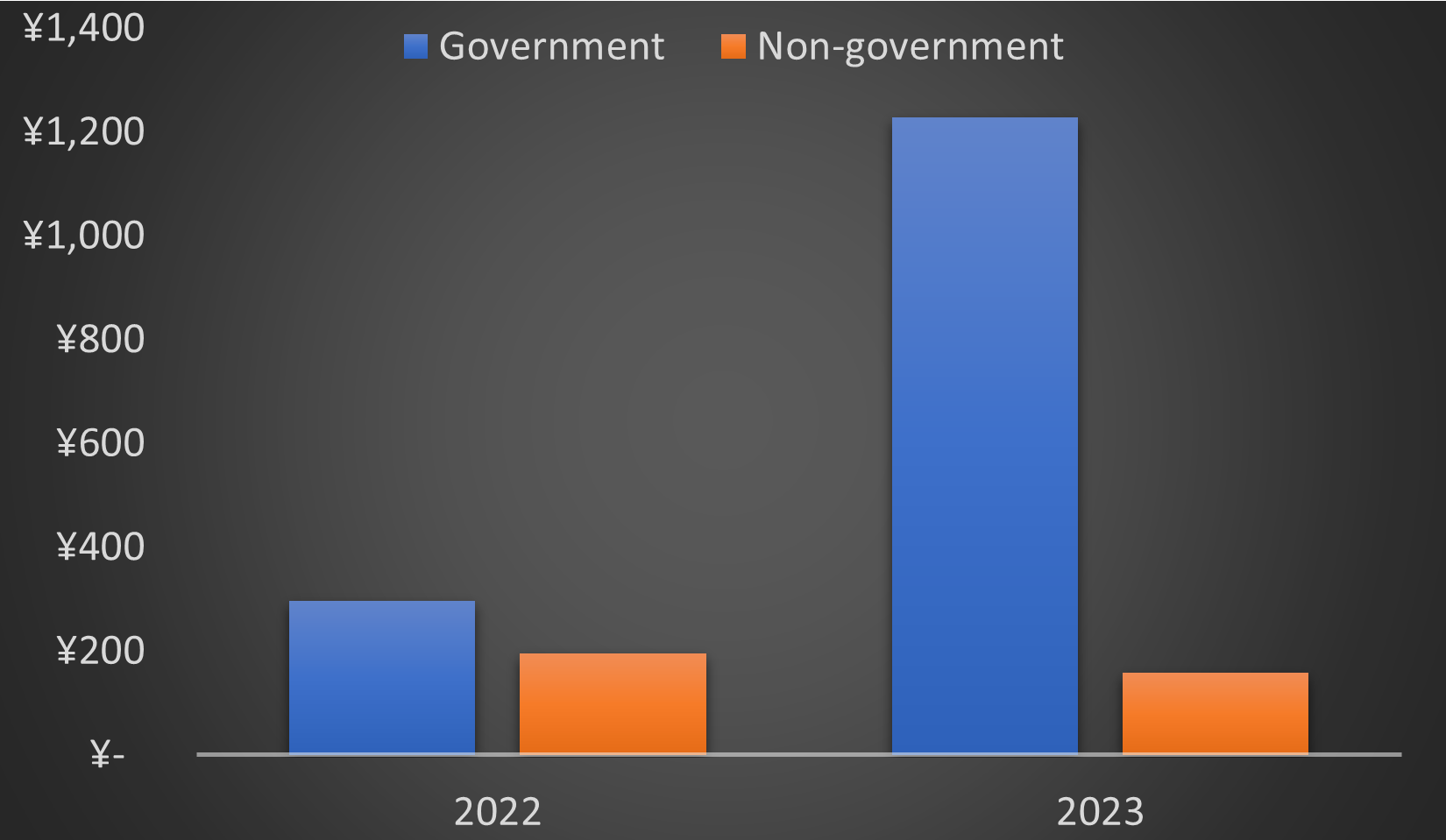

Synspective has for two two years sourced the majority of revenue from government customers. Commercial revenue actually shrank from 2022 to 2023. In 2023, Government revenue expanded to comprise 88% of total revenue. This likely matches the rest of the industry. The primary buyers of SAR imagery are governments (led by the U.S.). The only other public SAR company – iQPS – also reports its revenue is all government-sourced.

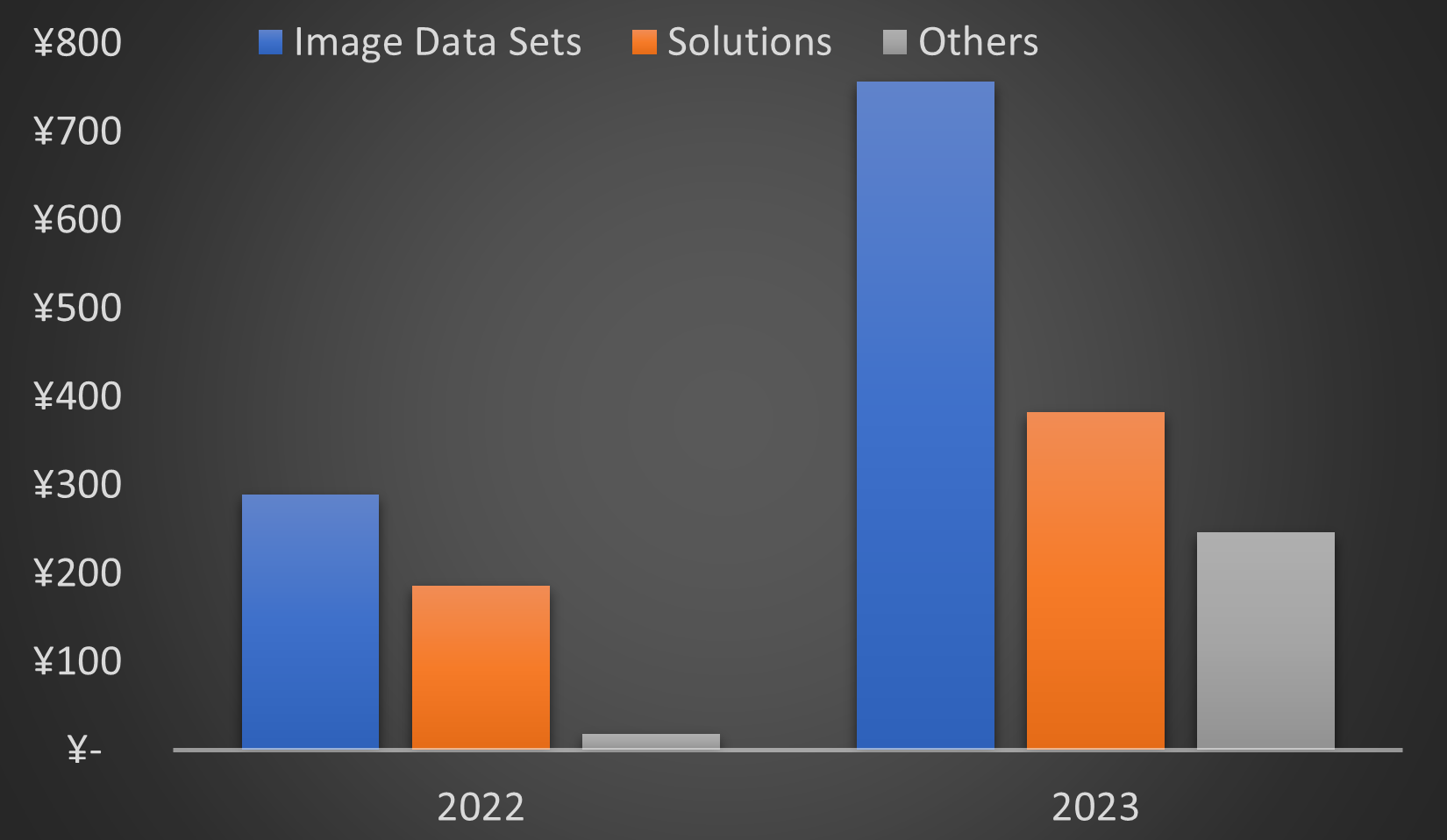

Synspective operates three main revenue segments – imagery data, solutions, and “other”. Imagery is self-explanatory, sales of imagery and customers. Solutions revenue encompasses Synspective analyzing imagery with software and providing resulting data analysis to customers. Solutions include monitoring changes at a specific location (like a construction site), accessing flood damage, and detecting illegal logging. Other revenues mainly come from contracted services related to satellite development and demonstration performed for government customer(s).

Business Economics

Synspective forecasts its seventh satellite will cost ¥2.83 billion, including launch. (Synspective contrasts this with 32b yen, the amount the Japanese government paid for a recent conventional SAR satellite.) According to Synspective’s business plan, satellite eight will cost ¥2.45 billion. And Synspective budgets ¥2.5 billion for each satellites nine through twenty. Synspective’s investor materials reveal Synspective pays about ¥1.1 billion to launch each satellite.

Thus Synspective pays about $9.4 million to make each satellite. With launch cost included, they spend about $16.8 million total to deploy one satellite. Contract with each of their four competitors:

- iQPS reported the cost to develop, build, launch, and insure one satellite is approximately ¥1 billion ($6.7 million). This is 60% discount to Synspective’s cost, all though Synspective apparently tops iQPS with better resolution.

- Capella Space cost to build and launch is “in the single-digit millions,” according to CEO Payam Banazadeh. This a at least 40% less than Synspetive.

- ICEYE’s satellites cost $2m apiece to make, approximately 75% less than Synspective’s build cost.

- Finally Umbra’s cost is in the “low single digit millions” for each satellite. Umbra thus for a cost lower than Synspective offers a satellite with higher performing resolution. Their 16cm resolution SAR imagery is the highest commercially available.

Synspective’s third generation satellites launching 2026 and onward will have capacity to take 30 images a day. Synspective models selling each image for between 300,000 and 500,000 yen. Current Synspective reports selling 31.1% of its current imagery capacity. Their business model relies on selling 20-40% of total near term imagery capacity. Assuming five year mission and 20% of imaging capacity sold, forecasted revenue-per-satellite calculates to between ¥3.3 and ¥5.5 billion. Because each satellite costs ¥2.5 billion to make and launch, the numbers are there. Even if Synspective hits the bottom of both its sales quantity and sales price metrics, each satellite can operate profitably.

Per Synspective’s mid-term forecast, they plan deploying 11 satellites by 2026 end capable of generating 140,000 SAR imagery sets each year. They assume selling 20-40% of these imagery sets, with 80% of sales to the Japanese Defense Ministry. As of December 2024, Synspective’s satellites were generating 10,800 imagery sets per year, of which Synspective was selling 31.1%. Selling 40% of 13X more imagery is an ambitious target. However, if they hit the bottom 20% target of their plan range and 80% of sales stem from the Japanese Defense Ministry, this equates to ¥8.4 billion in yearly revenue, with ¥6.7 billion sourced from the Japanese government. Japan’s current defense budget for procuring satellite imagery (SAR and optical) is ¥22.6 billion. So ¥6.7 billion in sales to MOD fits within current budget constraints.

Based on the above sales metrics and Synspective’s modeled business costs, Synspective models attaining profitability upon its constellation growing to 10 satellites. Synspective plans to reach this by end of 2026.

Synspective’s business model ultimately aims for a constellation of 30 satellites, each generating of 40 SAR images daily, and selling 30% of these images. Synspective models reaching this in 2028. This is 438,000 SAR images generated yearly, equaling ¥39.4 billion in revenue at ¥300,000 per image. Synspective warns of downward price pressure, but writes imagery analytical services will make up for lower prices. In 2028, Synspective projects Japanese MOD’s share of revenue contribution decreasing from 80% to 60%. Per the above, this necessitates MOD procuring ¥23.6 billion of imagery and analytical services from Synspective.

Even if the entirety of MOD’s budget is directed towards buying Synspective’s SAR imagery and services, MOD’s satellite imagery budget still needs to grow beyond its current level to support Synspective’s business plan. MOD also procures optical imagery, so to sustain continued baseline purchases, MOD’s budget would need to double.

Finally, Synspective eyes U.S. government sales to reach its revenue targets. The U.S. government is the largest customer of SAR imagery. Synspective opened a U.S. subsidiary in January 2025. Unlike for optical imagery, the NGO does not limit procurement of satellite SAR imagery to U.S. controlled businesses.

Max profit valuation

If Synspective breaks even with 10 satellites and can build out and sell out its planed 30-satellite constellation with the same cost structure, a rough calculation of future potential probability may be performed. Above we calculated revenue per satellite over five years at between ¥3.3 and ¥5.5 billion, depending on image set sales prices. Using the low end, and noting Synspective claims ¥2.5 billion yen as cost to build and launch, this equates to ¥780 million profit per satellite over five years. 20 additional satellites yields ¥3.1 billion ($20.8m) profit per year at full 30 satellites constellation.

The above assumes Synspective sells 20% of their imaging capacity. Their own business model assumes selling 30% of acquired imagining capacity, which yields ¥4.7 billion in yearly profit ($31.2 million). Unless I am way off on math, Synspective as of writing already trades with a market cap of ¥77 billion, or 16.5x of these future projected earnings.

Management guidance scorecard

Synspective neither provides quarterly guidance nor multiple year financial guidance.

Synspective outlook and risk assessment

Among five industry SAR small satellite providers, Synspective has the highest satellite cost basis. As Capella, Umbra, and iQPS launch more satellites to build out their respective constellations, this added imagery capacity should produced downward price pressure. Synspective acknowledges this, but this will likely impact Synspective greater than competitors due to Synspective higher cost.

Synspective’s business plan is also contingent on significant growth of Japan’s MOD satellite imagery budget and MOD directing much of this budget increase towards Synspective.

What to look from Synspective

Synspective has an extremely ambitious plan to reach profitability after launching 10 satellites targeted for 2026. So many things must fall in place for this to happen.

- Synspective in 2024 was selling 31.1% of its imagery capacity. How does this number change as Synspective lauches more satellites and has more capacity to sell?

- Synspective models selling SAR imagery sets at 300,000 to 500,000 yen per. Does price erosion reported by Synspective (or its competitors) indicate average selling price will fall out of this range?

- Synspective long term plans to significantly supplement imagery sales with sales of analytics. Does “Solutions” segment continue growth?